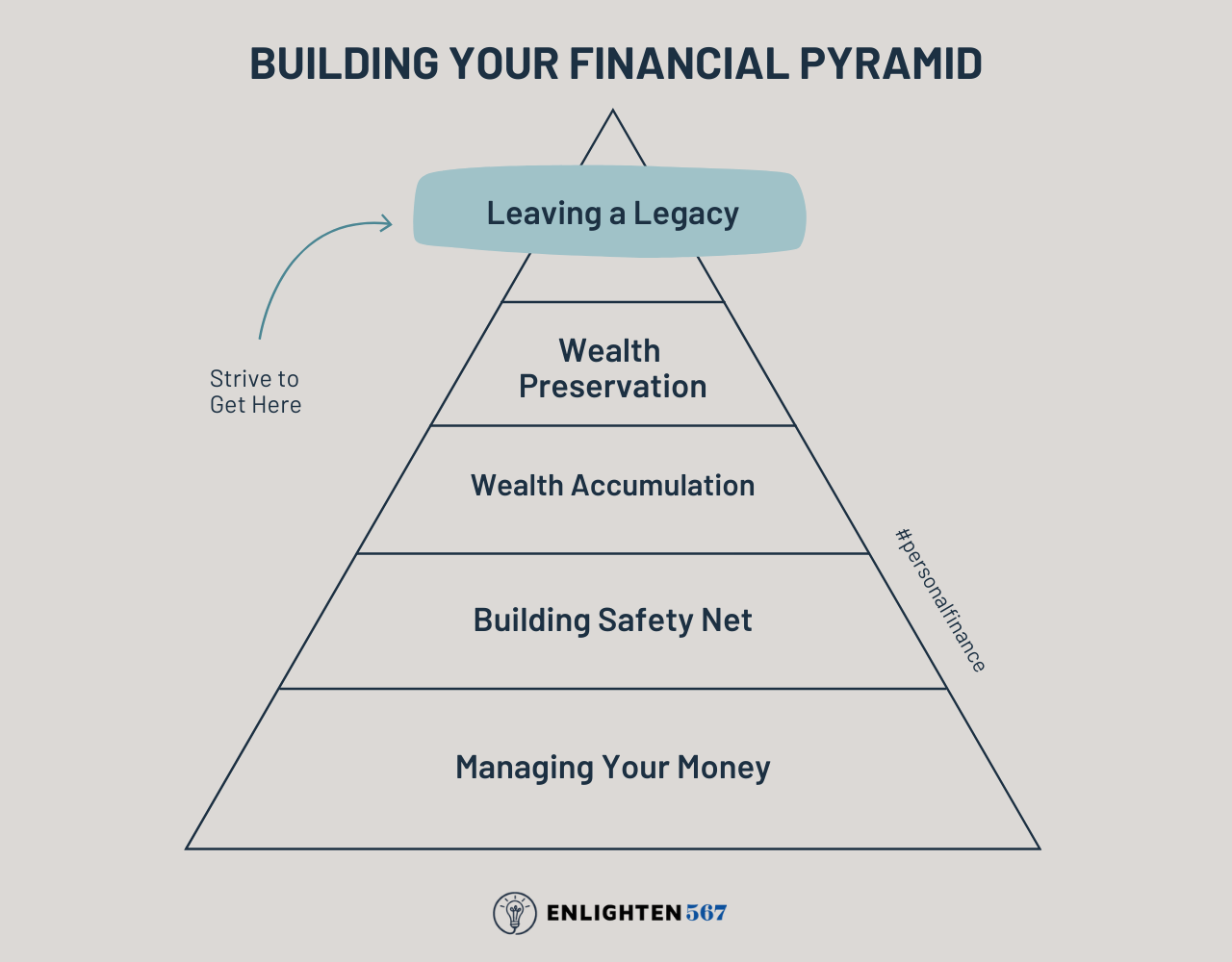

“What makes greatness is starting something that lives after you.” — Ralph W. Sockman

You’ve worked your whole life to grow your career, build a home for your family, put kids through college, and save for a fulfilling retirement. You look back and you feel proud of the hard work and sacrifices you’ve made to achieve your goals and offer your family financial stability.

However, many people fail to consider what happens to their life-long work after they’re gone or incapacitated.

Who inherits your assets and possessions?

If you have dependents, what happens if you’re not able to care for them?

Who will handle retirement and other savings accounts?

Most of the time, if these questions are left unanswered, the state decides the fate of your legacy and your family, but this doesn’t have to be your case.

Through the process of estate planning, you have the opportunity to figure out these specifics while considering additional elements such as tax and health decisions. Let’s dive into all the details of estate planning.

What is Estate Planning?

Estate planning is the process of preparing tasks to manage an individual’s financial situation in the event of incapacitation or death. It involves determining how an individual’s assets will be preserved, managed, and distributed.

Estate planning is not just for the wealthy, as anyone with measurable assets should consider it. Its goal is to streamline the management and transfer of property with the least financial and emotional burden on the family. This includes efforts to minimize estate-related taxes, manage asset distribution, and provide protection for loved ones in the event of death.

It is an ongoing process that should ideally be started once someone has measurable assets or a family and should be reviewed and updated to align with changing circumstances.

This process involves:

- Making a will

- Setting up trusts

- Naming an executor and beneficiaries

- Setting up funeral arrangements

And many other details that you can prepare with your financial professional and estate planning attorney.

Why is Estate Planning Important?

Estate planning is crucial for ensuring financial stability for you and your loved ones. Here are some of the reasons why creating an estate plan is important:

- Asset distribution: Estate planning allows you to decide who will inherit your assets and possessions according to your wishes.

- Protection from taxes: It helps mitigate the tax burden on your heirs, helping your assets transfer with the smallest possible tax impact.

- Family protection: Estate planning enables you to name guardians for your children and dependents, providing for their care in the event of your premature death.

- Avoiding family conflict: A well-structured estate plan can minimize the chances of family disputes and legal battles over your assets.

Many people overlook estate planning because they believe it’s only for the wealthy or think it’s too complex. However, consulting a financial professional along with an estate planning attorney can help kick-start this process.

Families who navigate legal and tax procedures to claim inheritances without an estate plan often encounter avoidable difficulties. The stories of James Gandolfini and Prince serve as clear examples of the consequences of inadequate planning.

Lessons from Celebrity Estate Mistakes

James Gandolfini, known for his role as Tony Soprano, left only 20% of his estate to his wife, which was estimated to be worth around $70 million at the time of his death in 2013. The estate was hit with a massive tax bill due to its size which amounted to about 55%. This meant that over half of the estate’s value was lost to taxes, leaving less for the beneficiaries. (2)

This illustrates the importance of proper tax planning and comprehensive estate planning to minimize tax burdens and ensure the smooth transfer of assets to beneficiaries.

Similarly, Prince’s estate faced tax disputes and complexities due to the absence of a will. Legal battles ensued among his six half-siblings, who were his legal heirs, lasting for over six years. (3)

These cases emphasize the need for everyone, regardless of estate size, to engage in proactive estate planning to secure their assets and provide for their loved ones.

Who Needs to Do Estate Planning?

72% of women and 59% of men do not have an estate plan, with the top reason cited being the belief that they don’t have enough money to warrant one. (1)

Estate planning is often seen as something only the rich need to worry about. However, this is a misconception. Everyone with assets, regardless of wealth, should have an estate plan.

Families of all economic standings must consider planning for unforeseen events impacting the family’s primary income earner. Without an estate plan, your loved ones may face significant challenges after your passing.

Let’s explore a common example:

You’ve worked hard to provide financial stability for your family, building a college fund, buying a house, and establishing a career to support their dreams. However, in the event of your unexpected absence, your family may face funeral expenses and the need to access your savings and retirement accounts to maintain their lifestyle and other expenses.

Without an estate plan, your loved ones may overpay taxes, undergo financial stress, or even have conflict and tension as they try to navigate forward without clear instructions.

Creating an estate plan is essential to safeguard your family’s financial future. By addressing potential challenges such as funeral expenses, tax implications, and accessing savings, you can ensure that your hard-earned legacy continues to provide stability and support for your loved ones.

Review the following questions to understand if you need an estate plan:

- Do you own a house or any other real estate?

- Do you have investments or other assets?

- Are you married?

- Do you have children?

- Do you have grandchildren?

- Do you have a retirement account or savings?

If you answered “yes” to any of the questions above, you may need an estate plan and by talking to a financial professional and estate planning attorney you’ll be able to start the process.

When to Start Estate Planning?

It’s best to start estate planning as soon as possible, ideally when you become a legal adult. However, it’s crucial to revisit and update your plan regularly, particularly when you have significant life events. Common life events that warrant prioritizing estate planning include:

- Marriage

- Birth or adoption of a child

- Buying a home

- An increase in wealth

- Medical diagnosis

Some other considerations include updating your estate plan before big trips, especially if traveling for long periods or frequently leaving the country.

Regardless of age, putting an estate strategy in place is important to ensure that family, financial, and medical affairs are taken care of in case of unforeseen events. Therefore, it is never too early to consider what would happen to your assets if you passed away.

How Does the Estate Planning Process Work?

The estate planning process can be broken down into manageable steps, typically involving the following key actions:

- Create an Inventory: Compile a comprehensive list of your assets and debts, including account numbers and contact information, as well as names and contact information for your important advisers.

- Account for Your Family’s Needs: Consider the needs of your family, including minor children and dependents, and make provisions for their care and financial well-being.

- Establish Directives: Create a last will and testament to specify who will inherit your assets after you pass away. You can also appoint guardians for minor children. As an alternative to a will, you can consider a living trust which allows for a more flexible and private distribution of assets.

- Review Your Beneficiaries: Ensure that you have named beneficiaries for bank accounts, retirement plans, and other assets to facilitate the transfer of these assets upon your death.

- Consider a Trust: Depending on your circumstances, consider setting up a trust to manage and distribute your assets according to your wishes.

- Make Health Care Directives: Create a living will and a power of attorney for health care to provide instructions regarding the medical care you wish to receive if you become incapacitated.

- Establish a Power of Attorney: Designate someone to act on your behalf if you are unable to do so.

It’s important to note that estate planning is not a one-time event, and it should be reviewed and updated regularly, especially after major life events such as marriage, divorce, births, deaths, and significant changes in financial circumstances.

Role of Professionals in the Estate Planning Process

Estate planning involves a team of professionals who work together to ensure your wishes are met and your loved ones are protected. Each professional brings specific experience to the table, guiding you through the process and ensuring a smooth transition for your beneficiaries.

Here are the key roles of professionals in estate planning:

- Estate Planning Attorney: They play a crucial role in drafting legal documents such as wills, trusts, and powers of attorney. They provide legal expertise to ensure that your estate plan complies with state laws and accurately reflects your wishes.

- Accountants and Financial Professionals: These professionals can provide tax planning, investment strategies, and financial management, ensuring that your estate plan maximizes the benefits for your beneficiaries.

- Life Insurance Agents: Life insurance agents can help you determine the appropriate amount of coverage to protect your family and estate, and they can also assist in integrating life insurance into your estate plan.

- Bankers and Brokers: They can aid in organizing and managing your financial assets, as well as coordinating the transfer of assets to your beneficiaries.

In addition to these professionals, individuals such as executors, trustees, agents, and guardians also play critical roles in the execution of an estate plan. It’s important to carefully consider the qualifications and responsibilities of these individuals when naming them in your estate planning documents. Regularly reviewing and updating your estate plan with the help of these professionals is essential to ensure that it continues to reflect your wishes and meets your evolving needs.

Estate Planning is an Ongoing Process

Estate planning is a not set-and-forget type of process, but rather a document that needs to be constantly updated and revisited on a timely basis.

Imagine this scenario: You’ve spent decades saving for retirement. You’re planning to leave a substantial sum to your spouse when you pass away. Yet, when that day comes, your money is automatically given to someone else, perhaps even your ex-spouse.

What happened? You forgot to change the beneficiary designation on your retirement account—a common estate planning error.

To prevent your assets from falling into unintended hands, it’s crucial to regularly review your plan and make updates as life events unfold and circumstances change.

Think of it like maintaining a car. Regular maintenance keeps it running smoothly, prevents costly repairs, and ensures a safe journey. Similarly, consistent attention to your estate plan ensures your wealth goes where you intend, protects your loved ones, and avoids unnecessary complications.

Secure Your Legacy Today

Navigating the intricacies of estate planning can be overwhelming with intricate details and legal considerations. While it’s essential to have a basic understanding to make informed decisions, you don’t have to tackle this alone.

Consider taking the next step toward legacy planning by seeking personalized guidance. Whether you choose to schedule a meeting with an estate planning professional or attend an educational webinar, these resources can provide you with valuable insights and a better understanding of how to create an effective estate plan.

By exploring these options, you can navigate the complexities of estate planning with confidence, ensuring your legacy is protected and your loved ones are secure.

Gain valuable insight at a no-charge attend an educational seminar or webinar near you

[su_divider]Sources:

(1) Fischer, Michael S. “Majority of Americans Lack Estate Plan, Health Care Power of Attorney.” ThinkAdvisor, 11 Oct. 2022, www.thinkadvisor.com/2022/10/11/two-thirds-of-americans-dont-have-an-estate-plan-survey/.

(2) Erskine, Matthew. “Lessons to Be Learned from Failed Celebrity Estates.” Forbes, Forbes Magazine, 29 June 2021, www.forbes.com/sites/matthewerskine/2021/06/18/lessons-to-be-learned-from-failed-celebrity-estates/?sh=68d779637f69.

(3) Varak, Robert. “Prince’s Estate Mired in Tax Fight.” Law Offices of Robert J. Varak, 3 Nov. 2020, www.varaklaw.com/princes-estate-hits-the-irs-with-a-million-dollar-lawsuit/.

(4) Estate Planning Webinar – American Bar Association, www.americanbar.org/groups/real_property_trust_estate/resources/estate_planning/webinar_estate_planning/.

(5) Viewpoints, Fidelity. “Estate Planning Made Easy.” Fidelity, 29 Nov. 2022, www.fidelity.com/viewpoints/wealth-management/estate-planning-made-easy.

Recent Comments